As you may aware the parliament has passed the new penalty regime for Self-managed Superannuation Fund (SMSF). Under the new legislation, ATO will gain the power to issue on the spot fines, directly and personally, to SMSF trustees using a range of penalties to match the seriousness if an offence.

As you may aware the parliament has passed the new penalty regime for Self-managed Superannuation Fund (SMSF). Under the new legislation, ATO will gain the power to issue on the spot fines, directly and personally, to SMSF trustees using a range of penalties to match the seriousness if an offence.

The new regime also increases the SMSF fines from $110 to $170 per penalty unit, or increased by 55%. ATO has indicated that each reported offence will automatically generate a penalty notice on each trustee.

This will put individual trustees to a disadvantage situation compare to a corporate trustee, as each trustee will bear the fines individually.

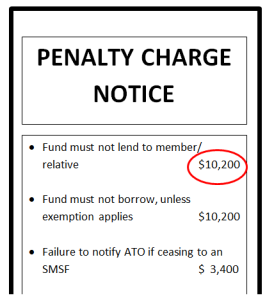

For example, a contravention report is reported to ATO due to lending money to a member or a relative (a serious breach of section 65(1)). This will attract a fine of 60 penalty points, or $10,200 (60 x $170).

If the trustee is a corporate trustee, then only the company will get the fine of $10,200. On the other hand, if the fund is individual trustees with 3 members, then each member may get a fine of $10,200, or a total fine of $30,600.

Another thing is the fines have to be paid from the trustees’ pockets and not from SMSF funds. These fines are not deductible and ATO may require the trustees to attend specific education for trustees or even freeze the assets of SMSF.

Trustee(s) may apply to waive the fines. ATO may waive or reduce the SMSF fines based on past history and seriousness of breach. ATO also may order the trustee(s) to:

• Rectification direction (sec. 159) – a written order by ATO to trustees to correct their wrong-doing within specified time period. For example, ATO may direct trustees to sell their property (if they were not prepared to this voluntarily).

• Education direction (sec. 160) – a written order to trustees to attend a specified course of education within a specified time period.

Below is some penalty guidance that may be imposed by ATO:

| Section | Description | Penalty Units | Penalty of each trustee |

| 160(4) | Failure to comply with Tax Office education direction | 5 | $850.00 |

| 124(1) | Failure to appoint an investment manager in writing when one is appointed | 5 | $850.00 |

| 254(1) | Failure to provide information to regulator on approved form | 5 | $850.00 |

| 347A(5) | Failure to complete a form with requested information as part of ATO’s survey | 5 | $850.00 |

| 35B | Failure to prepare financial statements | 10 | $1,700.00 |

| 103(1) & (2) | Failure to keep trustee minutes for at least 10 years | 10 | $1,700.00 |

| 104 (1) | Failure to keep records of change of trustees for at least 10 years | 10 | $1,700.00 |

| 34 (1) | Failure to follow prescribed standards | 20 | $3,400.00 |

| 106A(1) | Written notice to ATO if ceasing to be an SMSF | 20 | $3,400.00 |

| 65(1) | Fund must not lend to member/relative | 60 | $10,200.00 |

| 67(1) | Fund must not borrow, unless exemption applies | 60 | $10,200.00 |

| 84(1) | Fund must not breach in-house asset rules | 60 | $10,200.00 |

| 106(1) | Failure to notify ATO of significant adverse events immediately | 60 | $10,200.00 |