Should I Lodge Tax Return By Myself?

Lodging tax return? … It is the tax season again. Your mind is wondering how you should[…]

FREE Accounting Software – WAVE

A client introduced me to an accounting software. It is not a trial software. It is fully[…]

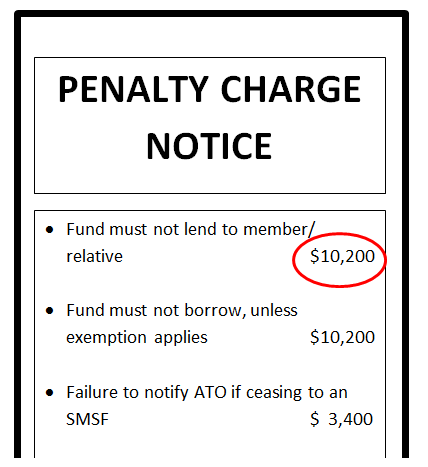

‘On the spot Fine’ is on The Way

As you may aware the parliament has passed the new penalty regime for Self-managed Superannuation Fund (SMSF).[…]

Managing Your SMSF

One of trustee key responsibilities is managing your fund’s investments. The investment decisions should be designed to[…]

Setting up An SMSF

Your SMSF needs to be set up correctly so that it’s eligible for tax concessions, can pay[…]

SMSF – Advantages & Disadvantages

An SMSF can become a powerful vehicle for your retirement. We include some advantages and disadvantages of[…]

Amending Your Tax Return

After lodging your tax return you may realise that there are some information that you forget to[…]